What is 'Risk'?

Explain it to me like I’m 5 year old.

Imagine you have a favorite toy, and you like to play with it outside. There’s a chance that something might happen to your toy while you’re playing—maybe it could get dirty, or it could break. That chance of something going wrong is called “risk.”

Now, in the context of banking, let’s think about a bank like a big toy chest where lots of people keep their money safe. But, just like how there are risks to your toy, there are risks to the bank’s money too. For example:

Market Risk: This is like if the bank’s money was in a lemonade stand, and suddenly it starts raining. People won’t buy lemonade in the rain, so the bank might not make as much money. In real banking, market risk means the value of investments might go up or down because of changes in the market.

Credit Risk: Imagine if you let a friend borrow your toy, and you’re not sure if they’ll give it back. That’s a risk you take. For banks, credit risk is when they lend money to people or companies, and there’s a chance they won’t get it back.

Operational Risk: This is like if your lemonade stand accidentally spills all the lemonade because the table wasn’t set up right. For banks, operational risk is when something goes wrong in their day-to-day operations, like a mistake or a system failure.

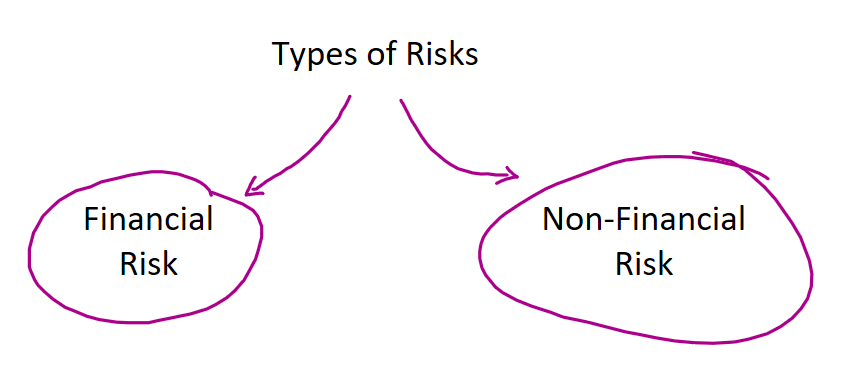

Let’s talk about the two main types of risks that banks and other financial institutions face:

- financial risks and

- non-financial risks.

Financial Risks

Financial risks are directly related to the money and investments of the bank. Here are the main types:

Credit Risk:

What It Is: The risk that borrowers won’t repay their loans.

Example: If someone borrows money to buy a house but can’t make the payments, the bank might lose money.

Market Risk:

What It Is: The risk that the value of the bank’s investments will change due to market conditions.

Example: If the bank has invested in stocks and the stock market crashes, those investments lose value.

Liquidity Risk:

What It Is: The risk that the bank won’t have enough cash to meet its short-term obligations.

Example: If too many people want to withdraw their deposits at the same time and the bank doesn’t have enough cash on hand.

Interest Rate Risk:

What It Is: The risk that changes in interest rates will affect the bank’s earnings.

Example: If the bank has to pay more interest on its borrowings but can’t charge higher interest rates on its loans.

Operational Risk:

What It Is: The risk of loss due to failed internal processes, people, and systems.

Example: A mistake in processing transactions or a bank computer system failure.

Non-Financial Risks

Non-financial risks are not directly related to money and investments but can still have a big impact on the bank. Here are the main types:

Operational Risk:

What It Is: Similar to the financial side, but more broadly includes risks from internal failures.

Example: Fraud, system breakdowns, or human errors.

Compliance Risk:

What It Is: The risk of legal penalties, financial forfeiture, and material loss a bank might face when it fails to act per industry laws and regulations.

Example: If a bank doesn’t follow anti-money laundering laws and gets fined.

Reputational Risk:

What It Is: The risk of damage to the bank’s reputation, which can affect customer trust and loyalty.

Example: If a bank is involved in a scandal, people might not want to do business with it anymore.

Strategic Risk:

What It Is: The risk that a bank’s business strategy might fail.

Example: If a bank decides to expand into a new market but doesn’t succeed, it could lose a lot of money.

Environmental and Social Risk:

What It Is: The risk related to environmental and social factors that can impact the bank’s operations and reputation.

Example: If a bank funds projects that harm the environment, it might face backlash from the public and regulatory bodies.

So, financial risks are directly tied to money and investments, while non-financial risks are more about the operations, regulations, reputation, and strategy of the bank. Both types of risks are important for banks to manage carefully to ensure they stay safe and profitable.

Okay!But how do I relate it with a bank?

Let’s understand a bank’s balance sheet. A balance sheet is like a report card for a bank. It shows what the bank owns (its assets) and what it owes (its liabilities), along with the money invested by the owners (equity).

Assets (What the Bank Owns)

- Loans: These are like IOUs from people or businesses who borrowed money from the bank.

- Risk: Credit Risk – Some borrowers might not pay back their loans.

- Investments: These are things like bonds or stocks that the bank buys to earn money.

- Risk: Market Risk – The value of these investments can go up or down.

- Cash and Reserves: This is the money the bank keeps on hand, like the cash in a lemonade stand’s money box.

- Risk: Liquidity Risk – The bank needs enough cash to meet demands from depositors wanting their money back.

Liabilities (What the Bank Owes)

- Deposits: This is the money that people have put into the bank for safekeeping.

- Risk: Liquidity Risk – The bank must have enough cash available if many people want to withdraw their deposits at once.

- Borrowings: This is money the bank has borrowed from other sources, like other banks.

- Risk: Interest Rate Risk – If interest rates change, the cost of borrowing can increase.

Equity (Owners’ Investment)

- Shareholders’ Equity: This is the money invested by the owners or shareholders of the bank.

- Risk: Operational Risk – If the bank doesn’t manage its operations well, it might lose money, affecting the shareholders.

Ah! I get it now.

Credit Risk: Mainly related to loans. If borrowers don’t pay back, the bank loses money.

Market Risk: Mainly related to investments. The value of stocks or bonds can go up or down.

Liquidity Risk: Related to deposits and cash reserves. The bank needs enough liquid money to handle withdrawals.

Interest Rate Risk: Related to borrowings. If interest rates go up, the bank might have to pay more interest on its borrowings.

Operational Risk: Related to all parts of the bank. Mistakes, system failures, or fraud can affect the bank’s overall performance.

So, a bank’s balance sheet is a mix of things it owns and owes, and each part has its own risks that the bank needs to manage carefully.